Why selling into large accounts has stopped being a transaction and started being a coordinated act of change management — a Future of Selling research conversation with Accent.

Prof. dr. Régis Lemmens — Future of Selling — May 2026

There is a common picture of how staffing firms sell to large industrial customers. The salesperson visits the procurement office. Procurement asks about price per hour and service-level guarantees. A framework agreement is signed. Candidates flow. The relationship is operational, the conversation is transactional, and the differentiation — if any — sits in the margin and the speed of response.

If that picture was ever the whole truth, it is no longer. Over two long research conversations, Lien Byttebier, who runs the Dedicated Accounts business at Accent, described a sales model that bears almost no resemblance to the picture above. The customer she sells to is not a procurement office. It is a multi-level organisation with three separate buying logics, three separate languages, and three separate timeframes. And the work of selling to that customer is, increasingly, the work of coordinating change inside it.

Accent is the second-largest staffing company in Belgium. Their large-account business — sub-fifty million today, but where the next phase of growth sits — is a deliberate move out of the SME segment they have historically dominated. That move forced them to invent a sales architecture different from the one their regional offices use to dominate the SME market. The architecture they describe is, I think, one of the cleanest examples in the Future of Selling research programme of what consultative, system-level selling actually looks like in practice. What follows is what surfaced across the two conversations.

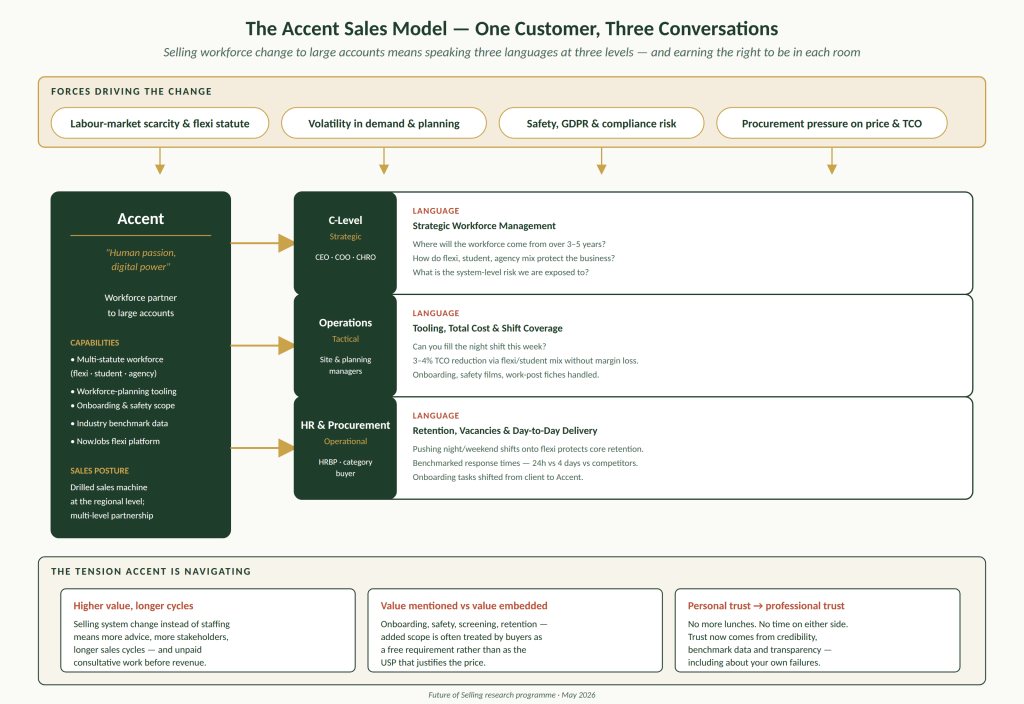

The picture above is the architecture. Above it sit the market forces driving the customer’s need to change. Below it sit the three commercial tensions Accent has had to learn to navigate as a consequence. The middle is where the actual work of selling happens — and the central insight is that it happens at three separate levels of the customer’s organisation, simultaneously, with three different propositions, told in three different languages, by three different people on the Accent side.

Why one salesperson cannot sell this

Accent’s first realisation in moving into large accounts was that the SME playbook does not survive contact with a corporate buying coalition. In an SME, the salesperson sits across from the owner or the HR manager and a deal can be closed in one meeting. In a large account, the procurement function holds the contract tightly — sometimes assisted by an external consultant — and that is, by Lien’s own description, the least pleasant kind of process to be in, because the conversation is structurally constrained to price.

The escape from that constraint is networking — but networking with intent. The Accent approach is to deliberately establish contacts at three distinct levels of the customer organisation, with each level addressed by a counterpart on the Accent side who has the title, the bagage, and the credibility to be in that conversation. At C-level, the strategic conversation about Workforce Management — where will your people come from in three to five years, and how do you protect the business against scarcity. At the operational tier, the tactical conversation about tooling, total cost, and shift coverage. At HR and procurement, the day-to-day conversation about retention, vacancies, and feedback loops.

This is not a soft preference. Lien was unambiguous that the conversation only works if the language fits the level:

“You have your title that helps you. It helps to bring certain messages. If you go to an HR Business Partner, you talk about how to fill vacancies. If you go to C-level, you can challenge — much more — how their process runs, how they see scarcity, how they think about it over the longer term. You cannot ask a consultant (salesperson) to have those conversations. It simply does not work. So you have to split it.”

She also flagged the converse — the moment that reveals the structural truth of the model:

“It is sometimes very strange, but I send the same sentence via LinkedIn to a person at a certain level as one of my colleagues does from their title. I get a response. They get no response. That is just how it is. You cannot give everyone a C-title.”

This is what the Future of Selling research has documented across multiple sectors as the buying coalition stretch. McKinsey’s number — ten to thirteen stakeholders involved in an enterprise decision — sits inside the customer’s organisation. Each of those stakeholders has a different problem, a different vocabulary, and a different conception of value. The supplier that walks into the relationship with a single salesperson speaking a single language is, structurally, addressing one stakeholder out of thirteen. The supplier that walks in with a mini-network mapped against the customer’s network — and trained to speak at each level — is in the conversation with all of them.

Accent has built that mini-network deliberately, and the operational evidence is in the routine. Sales plans are now constructed around three explicit messages — strategic, tactical, operational — with a named owner on the Accent side and a named counterpart on the customer side at each level. The deal is not sold by a salesperson. It is coordinated by a team.

The three languages, in practice

The interviews made the three propositions specific enough to be tested against. Each translates the same underlying capability — Accent’s multi-statute workforce platform combining traditional agency workers with the relatively new flexi statute and student labour — into a different value claim for a different audience.

To procurement: a Total Cost of Workforce conversation

The procurement counterpart hears the TCO story. If a customer shifts part of its workforce composition from traditional agency staff to flexi workers and students for nights and weekends, the total workforce spend drops by three to four percent — without Accent reducing its margin. The argument is not unit price. It is workforce mix engineering, with the cost reduction shown at the level of the customer’s full staffing budget.

To operations: a tooling, planning and onboarding conversation

The operations counterpart hears the planning story. Customers are increasingly receiving production plans at four in the afternoon for the next morning. They need ten people in an hour. The Accent answer is the planning tool, the integrated scheduling system, the multi-statute pool that can flex into night and weekend coverage, and the onboarding scope Accent has taken over — safety films, work-post fiches, worksite tours, medical checks. The conversation is procedural and concrete: can you cover the shift, and what does the handover look like?

To HR and the business: a retention and benchmark conversation

The HR counterpart hears the retention story. If the difficult shifts are absorbed by flexi workers and students who actually want to work evenings and weekends, the core agency population is no longer pushed into shift patterns they dislike — and core retention improves. And then, the part that genuinely surprised me when I heard it: Accent challenges the customer with benchmark data drawn from the rest of Accent’s own portfolio. Lien gave the example:

“We have ten large customers in logistics. Their average response time on a candidate presentation is twenty-four hours. Yours is four days. What do you think happens to the good candidates in that window?”

That sentence does work at three levels at once. It surfaces an unflattering fact about the customer’s own process. It does so with data the customer cannot dispute, because Accent has the comparison set the customer does not. And it shifts the conversation from “are you delivering candidates fast enough?” to “is your own process losing you the candidates we are delivering?” The Accent proposition stops being a service and becomes a diagnostic. And then, structurally, Accent has earned the right to propose changes to the customer’s process — onboarding, response loops, safety screening, retention — that are far harder to extract than candidates.

Trust has changed shape

The second interview made vivid a change that has been visible in the data for years but that few practitioners articulate as cleanly as Lien did. The kind of trust that B2B sales used to be built on — personal trust and likeability, the lunches and the long relationships — has not disappeared. It has been replaced as the primary mechanism by something quite different: professional trust, built on credibility, transparency, and demonstrated competence.

The reason is not ideological. The reason is that nobody has time anymore. Customer-side staff turnover has accelerated, contact persons rotate every two years on average, and the calendar room for relationship-building lunches has collapsed on both sides. Personal trust was always fragile against turnover; in a market where everyone turns over, the fragility has become structural. Lien put it concisely:

“Ten years ago a likability factor was key: I really take the customer’s time, we go to lunch together, we know things about each other privately, and that is how we build the relationship. I see today, certainly in Flanders and certainly in the large-customer segment, that I cannot get them to lunch anymore. They simply do not have the time. Trust now comes through authority. Through the fact that I bring something. That I help them advance.”

This is the shift from what the Future of Selling research has been calling the likeability model — buy from someone you like — to the credibility model — buy from someone whose judgement you trust. The argument is not that the new mode is morally superior. The argument is that the new mode is what the market structurally permits, given how little time anyone now has, how much rotation there is on both sides, and how saturated everyone is with sales contact.

What was most striking in the conversation was Lien’s account of how Accent actively constructs that professional trust — and the move is counter-intuitive. The mechanism is radical transparency, including transparency about Accent’s own failures. When something goes wrong — a safety film not shown, a system not working, a slow week — Accent calls the customer proactively before the customer notices. Most salespeople sweep it under the rug and hope it never surfaces. Accent does the opposite:

“I have the strongest relationships with the customers where something has really gone wrong, where we picked up the phone ourselves to say: this has happened, our process failed, here is what we are doing about it. You could perfectly cover it up. But if you communicate proactively, you build something else. And then, paradoxically, you also earn the right to be a little arrogant — to put the ball back in the customer’s court when their process is the one that is failing.”

This is the inversion. The traditional sales model treats trust as a function of telling the customer good news. The Accent model treats trust as a function of telling the customer the truth — including the parts of the truth that reflect badly on Accent. The bet, and it appears to be paying off, is that customers are now sophisticated enough to recognise that a supplier who reports their own failures is also a supplier who will tell the customer their failures. And in a market where the customer’s own process is increasingly the binding constraint on commercial performance, that diagnostic capacity is the value.

The tension at the heart of the model

None of this is free. The Accent model is structurally more expensive than the SME playbook it replaces, and the second interview surfaced the central tension that any supplier moving into system-level selling will eventually run into. Lien named it directly:

“If you can take the customer along very early in the change and offer solutions for that change, you are in a good place. The downside is that your sales cycle becomes longer and more complex. You are doing a lot of advice, a lot of consultative work, before you might or might not get to a sale. And the price pressure today is still high. You need high-level sales, long sales cycles, and you have to deliver a lot of added value before you invoice a single euro.”

This is the price of the model. Selling at the strategic workforce level means engaging customers months — sometimes years — before they have an active staffing requirement. The flexi statute extension to most sectors, due in mid-2026, is the kind of event Accent has been preparing customers for since 2024. Conversations begin with: this is coming, you will have to do something with it, your unions will resist, here is what we are seeing in other customers. Those conversations are unbillable. They are also, demonstrably, the work that wins the deal when the deal eventually materialises.

The structural answer is segmentation. The Accent model is not deployed uniformly across the customer base. The regional sales operation — which serves the SME segment and is where the company built its market position — runs as what Lien called a “drilled sales machine.” Sharp pitch, fast cycle, repeated sales training, sales competitions, examination, the works. The large-account model is the opposite — slow, consultative, multi-level, long-cycle. The two coexist because the customer behaviour they address is different. The regional buyer wants a fast match at a fair price. The large-account buyer wants a partner who can navigate a five-year workforce transformation. Asking one salesperson to do both, in Lien’s view and in mine, does not work.

The second commercial tension is more subtle. Accent has taken over genuine value-creating scope from its customers — onboarding, safety screening, work-post familiarisation, retention follow-up, GDPR compliance, candidate screening for safety mindset. Each of these is real work, with real cost, that delivers real value. But in the customer’s procurement worldview, this scope is often treated as a “requirement” that should be delivered at the same price — not as a USP that justifies a price premium. Lien acknowledged the trap, and named the fix:

“That is something we have to push forward more — proactively saying: look, we do all this to reduce the risk of workplace accidents, to handle GDPR, to manage your onboarding. That has to become a USP. Not a hygiene factor.”

This is, again, the Future of Selling research pattern visible at close range. Value that is delivered but not embedded in the proposition is value that procurement does not pay for. The Layered Business Case discipline — naming each dimension of value the supplier delivers, assigning it a stakeholder owner, attaching evidence, and putting it on the same page as the price — is the structural fix. The fact that Accent recognises the gap is the precondition for closing it.

AI and the human renaissance

The second conversation closed on the question of AI, and the answer Lien gave was striking enough that I want to quote it at length. Accent’s internal framing is the phrase “human passion, digital power.” The digital part handles the administration — candidate data entry, intake forms, holiday certificates, the long tail of clerical work that used to consume consultants’ days. What that frees up is exactly the work that creates value with customers:

“If AI fills in the candidate forms for us, you might ask what’s left for our consultants to do. But that’s the wrong question. The point isn’t to replace people — it’s to free them up for the work that actually matters: calling a worker to ask how their first day went, walking a new candidate through the worksite, sitting down with a customer to figure out why their response times are slow. That work becomes more interesting, not less. And it’s the part AI can’t do. That’s what stays human.”

This is the cleanest articulation of the Future of Selling Trend 4 I have heard from a practitioner. AI is not a threat to consultative selling. AI is the precondition for consultative selling at scale, because it removes the administrative weight that was always the reason consultants did not have time to do consultative work. The job is not eroding. The job is being purified down to the parts that always created the real value — judgement, presence, translation, trust-building across a coalition — and the parts that never did are leaving.

What suppliers across industries should take from this

Accent operates in a hyper-mature market — labour services, large-account segment, in a slightly contracting industry where several mid-tier competitors will not survive the next eighteen months. The pressures Lien described are not unusual; the response she described is. Five things from these two interviews are, I think, transferable to any supplier selling into large-account B2B in industrial Europe right now.

- The customer is no longer a single counterparty. Stop building your sales process around the procurement contact. Map the three levels of decision-making — strategic, tactical, operational — and assign Accent-side counterparts who can credibly converse at each. Sales is no longer a person. It is a coordinated team move.

- Each level needs its own value proposition, translated into its own language. The TCO conversation belongs to procurement. The tooling and onboarding conversation belongs to operations. The retention and benchmarking conversation belongs to HR. The strategic workforce conversation belongs to the C-suite. The same underlying capability has to be re-expressed three times. Do not collapse the messaging into one slide deck and expect it to work.

- Trust is now built through credibility, not chemistry. The lunch is dead. What replaces it is industry benchmark data the customer does not have, transparency about your own failures, and the credibility that comes from being more rigorous about your own performance than the customer is about theirs. The supplier that calls to report their own failure is the supplier the customer trusts to tell them the truth about their own.

- Consultative selling is now structurally unpaid up-front. If your business model cannot absorb six to eighteen months of advisory work before revenue, you are not in the large-account market. The segmentation question — with which customers is consultative selling worth the up-front investment — has become the most consequential commercial decision a supplier makes. Get it wrong and you will deliver enterprise selling at SME prices, which is the failure mode I see most often in the research.

- Embedded value beats mentioned value. Every supplier in this market is doing more for their customers than they used to. The ones winning are the ones who explicitly name every additional scope they have absorbed — onboarding, safety, GDPR, retention, compliance — as a USP rather than as a free hygiene factor. The Layered Business Case discipline is the structural mechanism for doing that. The supplier who builds it wins; the supplier who keeps the value buried in goodwill loses on price.

The final pattern

Across two interviews and roughly three hours of conversation, the through-line of the Accent story is this. Selling into large industrial customers is no longer the act of delivering a service. It is the act of orchestrating a change inside a customer organisation that has too many stakeholders, too little time, and too much pressure to absorb that change through traditional procurement channels. The supplier who shows up with a candidate and a price quote is selling something the customer has already commoditised. The supplier who shows up with three conversations, three propositions, three counterparts, and the credibility to be in each room is selling something the customer cannot get from a procurement portal — and is, increasingly, the only kind of supplier the large-account market is buying from.

The model is harder. The cycle is longer. The investment is bigger. The pre-revenue advisory burden is real. But the prize at the other end of it is not a deal. It is a partnership inside a customer’s organisation that competitors cannot displace without rebuilding the same multi-level architecture from scratch — and most of them will not. The next five years of large-account B2B will be won by the suppliers who recognise that selling has become change management, and who have built the operational infrastructure to do that work at scale. Accent has, and the conversations with Lien are the clearest practitioner articulation of what that infrastructure looks like that I have heard in this research programme.

This article draws on two Future of Selling research interviews conducted with Lien Byttebier, Commercial Lead for Dedicated Accounts at Accent. The full working paper From Value Selling to Value Engineering is available at futureofselling.eu.

Leave a comment