What a Japanese chemicals firm in Westerlo is teaching us about matching supply with demand in a world that no longer behaves predictably.

Prof. dr. Régis Lemmens — Future of Selling — May 2026

There is a story about the future of B2B selling that focuses on the salesperson — on what they say, how they pitch, which questions they ask, how they handle objections. That story is real, and I have written some of it. But I spent an afternoon last week with a senior procurement and supply chain leader at Kaneka Belgium, and I came away convinced that the more important story for industrial Europe right now is not about how salespeople talk. It is about how supply chains breathe.

Kaneka makes polymers. Their plants in Westerlo produce the liquid base material for the sealants you buy in DIY stores, the PVC additives that go into window and door frames, and the expanded polypropylene beads that end up inside bicycle helmets, car bumpers, and Starbucks straws. Their customers are firms like Henkel, 3M, Soudal, and the tier-one automotive suppliers. Their suppliers are the largest petrochemical companies in the world: BASF, INEOS, LyondellBasell, Shell, Arkema. They sit, in other words, in the middle of one of the most consequential industrial supply chains in Europe — invisible to consumers, indispensable to almost every brand consumers do see.

That middle position is no longer the comfortable place it used to be. The market around Kaneka has stopped behaving the way industrial supply chains behaved for the forty years before 2020. And the way Kaneka has had to adapt — operationally, commercially, culturally — is, I think, the clearest picture I have yet seen of what the next decade of B2B will actually look like.

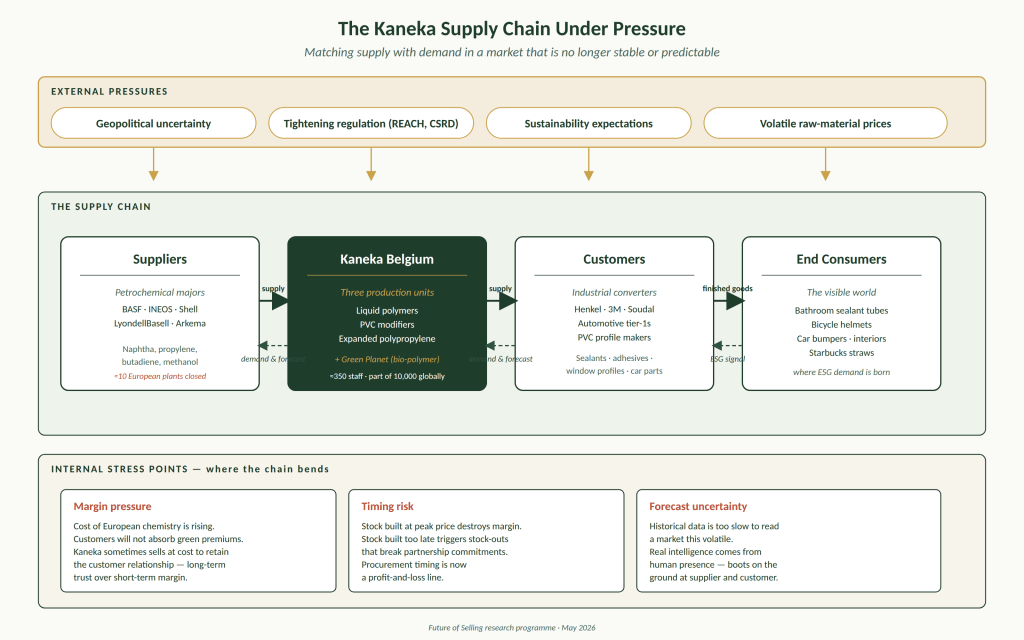

The picture above is the architecture. External pressures push down onto the supply chain itself; the supply chain pushes back through internal stress points that show up as margin compression, timing risk, and forecast uncertainty. What follows is the conversation behind each part of that picture, as it surfaced over three hours with someone who has spent thirty years operating inside it.

The pressures acting on the chain

Four pressures came up in the interview, and they were not framed as discrete issues. They were framed as a single environment the supply chain now has to operate inside.

Geopolitical uncertainty has become operationally arithmetic. Brexit, the Ever Given grounding the Suez, COVID, the war in Ukraine, and now the Iran conflict have stacked rather than resolved. The interviewee, who has run procurement at this scale for three decades, told me he has “never seen prices rise this fast.” When Asian petrochemical capacity went offline because of Iran-related disruption, butadiene flows reorganised globally, and European prices followed within days. Geopolitics is no longer a topic for the strategy department. It is a line item in next week’s raw-material cost.

Regulation is tightening on multiple fronts simultaneously. REACH continues to add restricted substances. CSRD reporting starts in 2027 for 2028 publication. A four-person regulations team is permanently allocated. US sanctions lists change daily and conflict with Chinese counter-legislation, which is why two legal advisers now sit full-time on trade compliance. The customs work is, in the interviewee’s words, “a hundred times harder than it used to be.”

Sustainability expectations have arrived without the willingness to pay for them. Customers ask for lower-carbon products, more recyclable products, products with documented lifecycle analyses. Kaneka has invested heavily in delivering exactly this — including Green Planet, a bio-based polymer that fully composts in eight weeks. The technology exists. The buyer who will pay the premium does not, yet. We will come back to this.

Raw-material prices have stopped being a curve and started being a series of step-changes. In the last five years, roughly ten European petrochemical plants of significance to Kaneka’s supply have closed — LyondellBasell’s Maasvlakte PO/SM unit, Vynova, and others the interviewee could list by name. More are coming. The European chemistry industry is shrinking, partly because of energy costs, partly because of Chinese competition, partly because of regulation. The remaining suppliers concentrate volume; pricing power moves with them.

None of these pressures resolves the others. They compound. And they all land on the same supply chain at the same time.

The relationship with suppliers

Global versus local sourcing — the choice you no longer have

I asked whether the regionalisation trend you read about in trade press was visible inside the company. The answer was carefully two-sided. “I would prefer to buy maximally European,” he said. “It is easier for me. I buy in Germany, I buy in Spain, and that is the end of it.” The problem is that the European chemistry footprint is contracting. Plants close. Capacity consolidates. Single-source exposure becomes the default, not the exception. Risk management forces sourcing across regions even when the operational preference is to stay close to home. The other reason is cost: European energy and labour have made some chemistries 20 percent more expensive than the Chinese equivalent. The procurement decision is no longer a simple optimisation. It is a permanent triangulation between proximity, resilience, and price.

The end of just-in-time as an article of faith

For the decade before 2020, stock was treated as a defect. Lean supply chains optimised it out. Suppliers told their customers — Kaneka included — that the supplier would carry the inventory and the customer should not need it. “Just-in-time,” the interviewee said with mild dryness, “was the term they came here to sell us.” COVID broke that arrangement. Suppliers cut their own stocks to save cost, the system went rigid, and when one container disappeared from the rotation the entire flow stopped. The pendulum is now swinging back. Stock is being rebuilt — sometimes for resilience reasons, sometimes for price-timing reasons, sometimes for both at once. The just-in-time orthodoxy has not been replaced with anything as confident. It has been replaced with judgement, exercised weekly.

Trust and relationship as commercial infrastructure

This is the part of the interview that would surprise nobody who has worked in Japanese-owned industrial companies — and would surprise almost everyone whose career has been spent in the spreadsheet-driven procurement cultures that dominated 2010s sourcing. The interviewee was unambiguous: Kaneka’s supplier relationships are partnerships, and they are managed as such over decades.

“In Japanese companies it is always customer intimacy and product quality at the top. Cost matters, but it is never the first thing. I have never met a Japanese firm that competes on cost alone. The same logic runs both directions — toward our customers and toward our suppliers.”

During COVID, when many firms in the chain raised prices opportunistically, Kaneka did not. Customers still remember. That memory is now a commercial asset Kaneka can draw on in a tight market. Partnership is not a culture statement; it is the inventory you draw down when conditions get hard.

Volatility demands intelligence — about availability, timing, and price

The single most operationally consequential statement in the interview was this: when you sit between volatile suppliers and volatile customers, the value-creating asset is not your stock. It is your information. Knowing which European plant is about to shut down, before the announcement. Knowing that butadiene is about to spike because Korean capacity is offline. Knowing which Tier-1 automotive customer is preparing to cut production next month and will therefore not need next month’s resin. Decisions about how much to buy, when to buy it, what to produce, and what stock to hold are now driven by intelligence that has a half-life measured in days.

That intelligence does not come from public data, from market reports, or — and this is the line worth highlighting — from AI summarising the internet. It comes from people in rooms with other people, exchanging what they each know. We will return to this point in the conclusion, because it is the most consequential observation in the interview for what selling and procurement actually become in the next decade.

The relationship with customers

Forecasting demand from inside the customer’s plant

When I asked about forecasting, the interviewee laughed gently. Forecasting, he said, is now an exercise in being closer to the customer than the customer is to their own forward plan. Historical-data forecasting tells you what was true last quarter. Public-data forecasting tells you what was true last week. Neither tells you what will be true on Monday. The intelligence Kaneka actually trades on comes from sales colleagues sitting in customer plants — looking at production schedules, reading body language, knowing whether the customer’s CFO is about to instruct a pause.

“You must have boots on the ground at the customer. Look them in the eyes. Ask what they will produce next week. The forecast is not on the internet. The forecast is in that room.”

Demand generation through innovation and co-creation

Kaneka’s R&D function has, in the interviewee’s own phrase, become R&B — Research and Business. The unit no longer pursues speculative chemistry programmes without a customer attached. Every project starts with a conversation in a customer plant — what they need to make next, what cost they need to take out, what regulatory horizon they are trying to clear. One concrete example came up: with automotive tier-one customers, Kaneka has been jointly designing a version of its expanded polypropylene bead that requires less energy to mould, because energy cost has become the squeeze point for the converter. The innovation is not Kaneka’s. The innovation is Kaneka and its customer’s, co-developed.

This is not a marketing claim. It is a structural change in where industrial innovation comes from. After a century of pushing inventions from R&D to customers, mature industrial firms have realised that the next innovations have to be pulled from the customer side. The work of demand generation is now indistinguishable from the work of co-creating what the customer will buy next.

The difficulty of supplying green solutions

This is where the story turns hard. Kaneka has, as I mentioned, developed Green Planet — a fully bio-based, compostable polymer. Eight-week breakdown in soil or seawater. No microplastic residue. Used by Starbucks in straws, in premium packaging, in horticultural clips that replaced the petroleum-based versions previously ending up shredded into farmland. It is a technically dominant product. And it is structurally difficult to sell at scale, for a reason the interviewee put plainly:

“I can easily find products that are better for the environment. My customer doesn’t want to pay for it.”

The customer signs the ESG report. The customer asks the supplier for the lower-carbon option. The customer’s procurement committee then compares the green product’s price against the petrochemical incumbent’s price and chooses the petrochemical incumbent. The technology has arrived. The willingness to pay has not. Kaneka has, in their phrase, put a substantial part of the green portfolio “in the fridge” — kept ready, kept available, waiting for the day a customer commits to paying for it. That day is coming. It is not here yet.

The structural fix to this is not to keep mentioning the environmental benefit more emphatically. The structural fix is to rebuild the business case so the environmental dimension lands on the same page as the price — alongside compliance exposure, lifecycle savings, strategic positioning, regulatory horizon, and reputational risk. That is the work the Future of Selling research programme has been documenting as the Layered Business Case, and it is the work that suppliers in industrial Europe will spend the next five years learning to do.

The conclusions worth holding onto

Aligning supply and demand is now an act of judgement, not a process

The cleanest expression of this came when the interviewee described what success looked like in the current market. The example: when raw-material prices peaked recently to unsustainable levels and then began falling, Kaneka had to time its purchasing so it did not lock in expensive raw materials that would later be converted into cheaper finished products. Buy too early, lose margin on the finished good. Buy too late, miss a customer commitment. There is no formula. There is judgement informed by intelligence. And sometimes — this is the part that surprised me — there is a deliberate decision to sell at cost in order to keep a customer supplied through a period of disruption.

“We continued selling through COVID when others raised prices. Our customers remember. The trust we built then is what we trade on now. We are not optimising for the short term. We are optimising for the partnership.”

This is the supply chain operating as a relationship system, not as a transaction system. The decisions that maximise next quarter’s margin are not the decisions that protect next decade’s commercial position. The supplier who understands this is operating in a different conversation than the supplier who does not.

The limits of AI, and what humans are actually for

I asked the interviewee directly about AI, because the question of where AI lands in B2B procurement is the question of our moment. His answer was the cleanest articulation I have heard:

“You can do what you want with AI. It will never replace what you do at a human level. AI will help. It can read historical data, surface trends, summarise information. But in turbulent markets that information is always too late. You must have boots on the ground. You must look the customer in the eyes. You must look the supplier in the eyes. And then you must decide.”

This is not a rejection of AI. He uses it. His team uses it. But the part of the job that creates commercial value — the part that determines whether the next twelve months are profitable or not — is the human part. Reading a meeting. Sensing whether a customer is about to fold. Building enough trust with a supplier that they call you before they call their other accounts. AI cannot do this work, and the work of AI inside procurement makes the human work more, not less, valuable, because there is less administration to hide behind.

Procurement and sales now operate as one team

One of the most concrete operational changes the interview surfaced is that the line between procurement and sales — which used to be a wall in most B2B firms — has functionally dissolved at Kaneka. The procurement leader joins his sales colleagues on visits to major customers. Sales colleagues join him on visits to major suppliers. Knowledge moves across the wall in both directions, and it creates value on both sides.

“If I take a salesperson with me to BASF, the salesperson tells the story about how we use the material in our customers’ applications. BASF hears it directly. That makes BASF a better supplier to us. It is a win for both sides. We do this in both directions now, and it is something we did not do five years ago.”

This is what an integrated buying coalition looks like from the inside. The McKinsey number — that ten to thirteen stakeholders are now involved in an enterprise deal — describes what is happening across firms. The Kaneka pattern describes what is happening inside one. The supplier who walks into a customer meeting with a sales-only proposition is walking into a customer organisation that has already integrated. The supplier who arrives with an integrated team — sales, procurement, technical, sustainability — is in the conversation. The supplier who does not, is not.

The structural infrastructure that makes all of this work

None of the above happens by accident. It happens because Kaneka has built a meeting cadence that locks the supply chain into the commercial conversation, weekly. Every two weeks, a sales meeting with each business unit. Once a month, a margin meeting that reconciles raw-material trajectories against pricing positions. Cross-functional reviews that pull in legal, regulatory, and operations as needed. Procurement is not a back-office function reporting upward at month-end. Procurement sits at the same table as sales, every week, looking at the same numbers, making the same decisions about which customers to prioritise, which suppliers to deepen with, and which deals to hold or walk away from.

This is the part of the picture that does not show up in the diagram. The diagram shows pressures and flows and stress points. What it does not show is the operational rhythm that turns those flows into commercial decisions every week, with the right people in the room, looking at the same information. That rhythm is the structural fix for everything else above it.

Risk management used to be compliance. Now it is the job.

The line that closed the interview, and that I think will close the next decade of B2B commercial practice, was this. For most of the careers of most of the people now running procurement and sales functions in industrial Europe, risk management was a compliance discipline — something the legal team did, something procurement filed at year-end, something everyone agreed was necessary and slightly tedious. It was treated as a tax on getting the real work done.

“Risk management used to be something we did because we had to. Today it is the day-to-day work. It is the work. Every meeting we have, every decision we make about a supplier or a customer or a stock position, is a risk decision. That is the change. It is the centre of the job now.”

This is the change. Not that risk is more important than it used to be — every generation of executives says that. The change is that risk has stopped being a separate function and become the operating system of supply chain management. When external pressures arrive in the firm with the velocity they now do — geopolitical, regulatory, environmental, financial — there is no longer a distinction between managing the operation and managing the risk. They are the same activity.

What this means for the supplier across the table

If you sell into industrial customers like Kaneka — or, more importantly, if you sell into the customers Kaneka sells into — the picture in the diagram is the picture of your buyer’s working week. The pressures on top are the pressures driving every purchasing decision. The stress points at the bottom are the lens through which every supplier proposition is now evaluated. Your offer is not being read against a procurement spreadsheet. It is being read against an environment of margin compression, timing risk, forecast uncertainty, and risk-management work that has become the centre of the job.

The supplier who shows up with a price quote is offering a one-dimensional answer to a multi-dimensional question. The supplier who shows up with a proposition explicitly designed to reduce the buyer’s exposure — supply risk, regulatory risk, reputational risk, lifecycle risk — is offering something the buyer is now structurally configured to value. That is not a marketing reframe. It is the recognition that supply chain pressure has become the centre of gravity of B2B selling, and that the supplier who organises around that recognition is operating in a market with very few competitors actually showing up there.

The Kaneka conversation is the clearest version of this I have heard in a year. It is not a story about a sales technique. It is a story about how industrial supply chains under pressure reorganise themselves around trust, intelligence, judgement, and integration — and about what suppliers have to look like to remain in the conversation when that reorganisation is complete.

This article draws on a Future of Selling research interview conducted in May 2026 at Kaneka Belgium. The full working paper From Value Selling to Value Engineering is available at futureofselling.eu.

Leave a comment